Still waiting for the libraries of your actuarial software to be updated for IFRS 17? Worried that those libraries will not be sufficiently flexible to cater for the nuances and allowable differences in approach under IFRS 17, especially as these differences can have a huge effect on your financial position? Need an independent system to ensure whatever output that comes from your actuarial department is accurate before using the figures in your accounts? Need a simple to use software which would allow you to understand and test the risks associated with IFRS 17 implementation for your risk management department? Need to price your products under IFRS 17 NOW to minimize adverse effects in 2021? A round of applause then for the A-PLOS actuarial software! Powerful enough for actuaries, simple enough for everyone to use.

Since 2011, Actuarial Partners has been actively developing and using models in the award winning Mo.net platform to perform a variety of actuarial work including valuation and pricing exercises. In 2018, we have taken a step further by enhancing our models to be able to perform IFRS 17 calculations. A-PLOS is designed for both conventional insurance and takaful businesses. More than just theory, A-PLOS is currently being used in our IFRS 17 work.

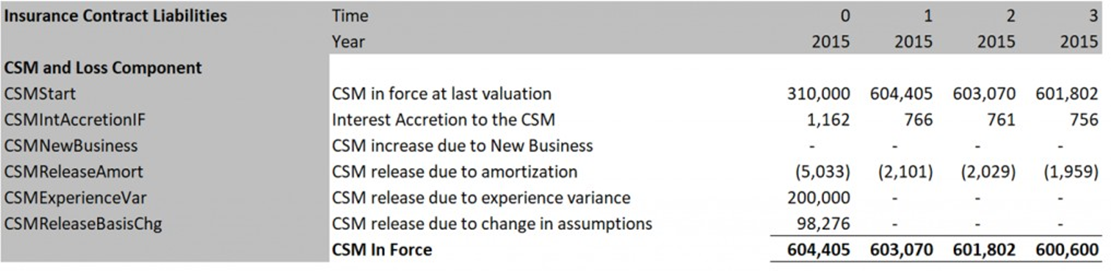

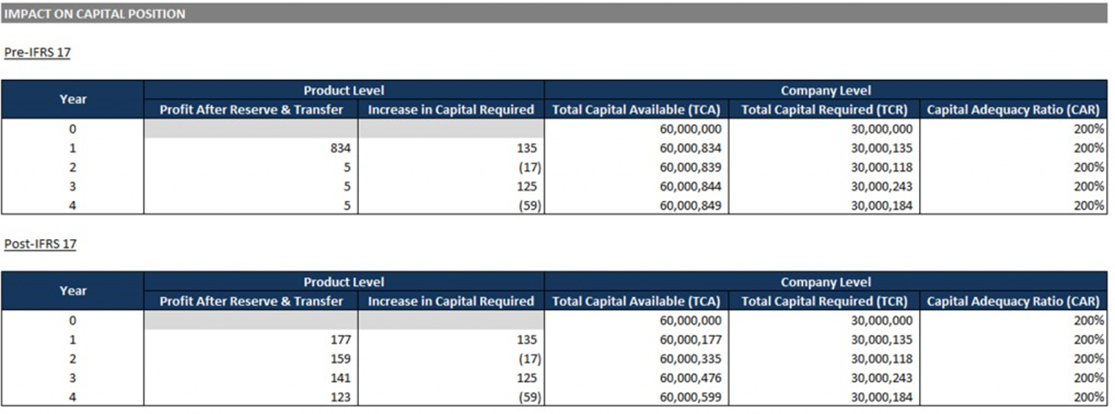

Apart from performing the liabilities calculations under RBC basis, the life office model now allows users to calculate IFRS 17 liabilities i.e. the Best Estimate Liabilities (BEL), Risk Adjustment (RA) and Contractual Service Margin (CSM) and also to perform quantitative impact study during the transition period. The model projects the P&L and balance sheet to allow users to better understand the profit signature under IFRS 17 environment. In addition, the model also projects the movement of CSM allowing for the interest accretion, variation in experience, and changes in assumptions based on the selected profit carrier.

For development of new products or repricing of existing products, we have developed an Excel based pricing tool with Mo.net as the backbone of the tool. This essentially means that users would only need to install a runtime version of Mo.net, at a significant discount compared to the full development version.

The pricing model is able to cater product development and pricing for a variety of products including non- participating e.g., term, endowment, annuity, mortgage reducing term and investment linked policies as well as variation in Takaful operating models (e.g., Wakalah or Mudharabah) for the Takaful business. Outputs include:

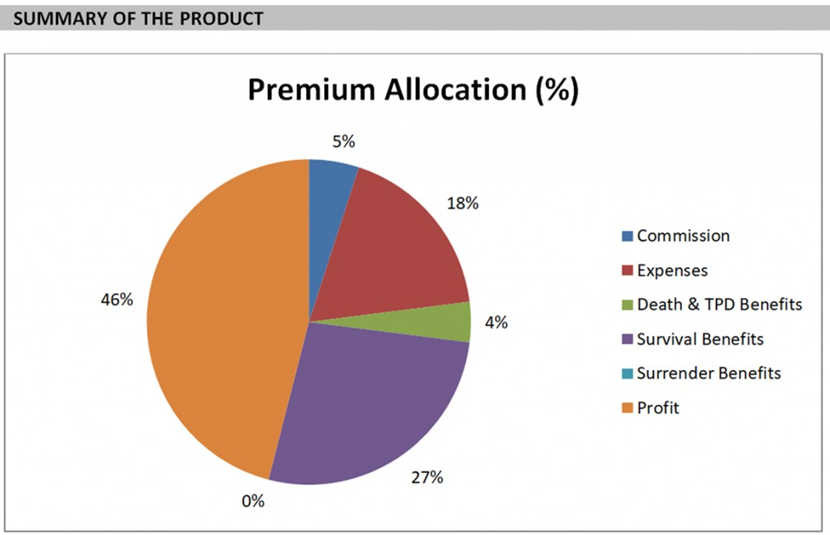

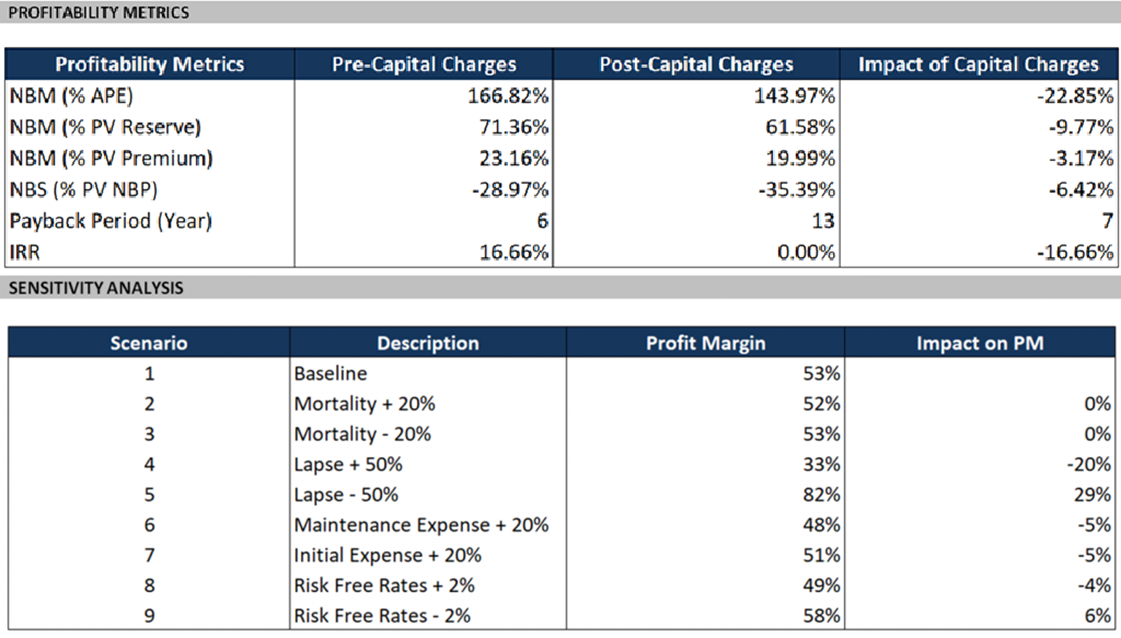

- key profit metrics such as profit margin, cost of capital, new business strain, payback period.

- sensitivity of profits to key assumptions

- new business financial projections

- documentation as per BNM submission requirements in their guideline “Introduction of New Insurance Products” including profit tests output on key ages and financial impact studies.

Furthermore, say goodbye to using modal points for pricing, A-Plos is able to utilize the “goal seek” function to ensure that the same profit margin is embedded for each age and duration.

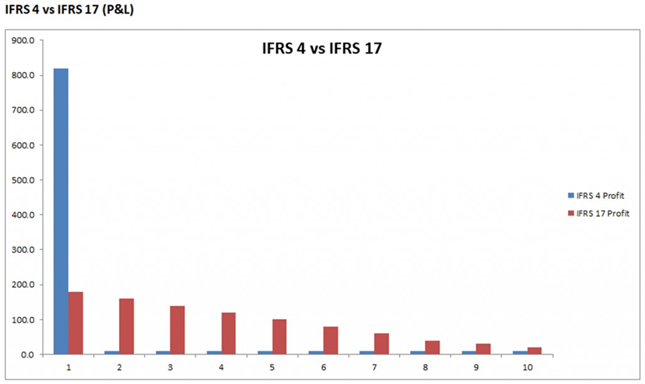

The pricing tool has built in functions to show the above analysis under IFRS 17. With this tool, insurers can start to reexamine their product line, or to develop new products that are more IFRS 17 friendly (in terms of profit emergence).

An additional consideration for the Takaful business has been given when setting up the IFRS calculations since the mortality risk is contained in the Risk Fund while the Operator Fund bears the expense risk. Both of these funds generate profits and since profits need to be systematically recognized over the duration of the contract under IFRS 17, A-PLOS has been designed to produce necessary calculations for IFRS 17 under 2 different scenarios i.e., one where there could be one CSM (similar to the treatment for conventional insurance), or another scenario where there are 2 CSMs calculated assuming the risk fund and operator funds are two separate accounts. Under the two CSMs approach, the model allows users to understand the drivers that significantly affect the movement of the CSM in both accounts (Risk Fund and Operator’s Account).